Health Insurance Claim Process - Cashless Claim & Reimbursement Claim

Learn about the health insurance claim process? Learn how cashless and reimbursement claims work, documents required, and tips to ensure quick claim.

Team Pazcare

This is some text inside of a div block.

Updated on:

November 7, 2025

Share

Table of Contents

Key Takeaways

A health insurance claim process is of two types, cashless claim and reimbursement claim. Let us dive deep into each of the claim processes. Find out how to claim in case of planned hospitalization. Know the documents required to raise and file cashless and reimbursement claims.

A health insurance claim process is of two types, cashless claim and reimbursement claim. Let us dive deep into each of the claim processes. Find out how to claim in case of planned hospitalization. Know the documents required to raise and file cashless and reimbursement claims.

What is a health insurance claim?

A health insurance claim is a request that a health insurance policyholder submits to a health insurance company to get the services mentioned in their health plan/policy during hospitalization or medical treatments. By sending this request, the health insurer is notified to initiate the claim process.

Types of claim in health insurance

There are two types of claim initiation in health insurance. They are cashless claims and reimbursement claims.

Cashless claim

As the name suggests, it frees us from handling money during medical emergencies. In a cashless claim, the insurer settles the medical bills directly to the hospital itself. This is applicable only if the policyholder is admitted to a network hospital. A network hospital is a hospital that has an agreement with the insurer to provide cashless treatment to the insured.

The policyholder or the insured can provide the details of the insurance policy taken along with the ID card provided by the insurer in the network hospital. After this the hospital will verify the details and submit the pre-authorization form to the insurer. Once the patient is discharged, the bills are sent to the insurer. The insurer verifies it and settles the bill to the hospital.

Hence, it makes you worry-free about settling the bills to the hospital.

Cashless claim during planned hospitalization

In the case of surgery, hospitalization is planned. Hence, the policyholder can avail cashless claims for planned treatments and hospitalization.

For availing of cashless claims, inform the insurance company beforehand. This is usually 4 days before the hospitalization.

Cashless claim for emergency hospitalization

For availing of a cashless claim for emergency hospitalization, you will have to inform the insurance company about the hospitalization to the nearest network hospital. Show valid proof that you hold the policy, for instance, a health insurance ID card provided by the insurer, and fill the necessary forms, you are good to go.

Reimbursement claim

In a reimbursement claim, once the insured is admitted to a hospital, the bills are paid from your pockets. Later, the insurance company will reimburse the claim amount to you once you provide the necessary documentation.

This is mostly the case when the policyholder goes to a hospital that is not in the network hospital list of the insurer. However, the claims are settled by evaluating the credibility of the documents you provide.

This is why it is important to choose an insurer with an extensive hospital network and a high claim settlement ratio. A claim settlement ratio suggests the percentage of claims settled by the insurance company to the policyholders in a financial year. The higher the ratio, the higher is the chance of your claims being settled.

Types of health insurance claims

Basis

Cashless claim

Reimbursement claim

Hospital Type

Network hospitals only

Any hospital

Who pays initially

Insurer

Policyholder

Claim Settlement

Directly between hospital and insurer

After documents submission

Processing Time

Faster

Longer (due to verification)

Ideal For

Planned/emergency hospitalization

Non-network hospital cases

Health insurance claim process

The health insurance claim process varies for a cashless claim and a reimbursement claim. Let us see how it is done.

Cashless health insurance claim procedure

The cashless health insurance claim procedure generally consists of the following steps

Firstly contact your insurer or you can contact the insurance help desk in the hospital.

Then, show valid proof like your health ID card - proof to show you hold a valid health insurance policy, unique identification card like a copy of Aadhar or driving license to the person in charge at the hospital.

After the verification process is complete, the hospital will submit the pre-authorization form provided by the insurer.

A few health insurers will assign field doctors to make the claim process easier for the insured.

After successful verification of the documents submitted, the claims will be initiated and settled according to the terms and conditions of your health insurance policy.

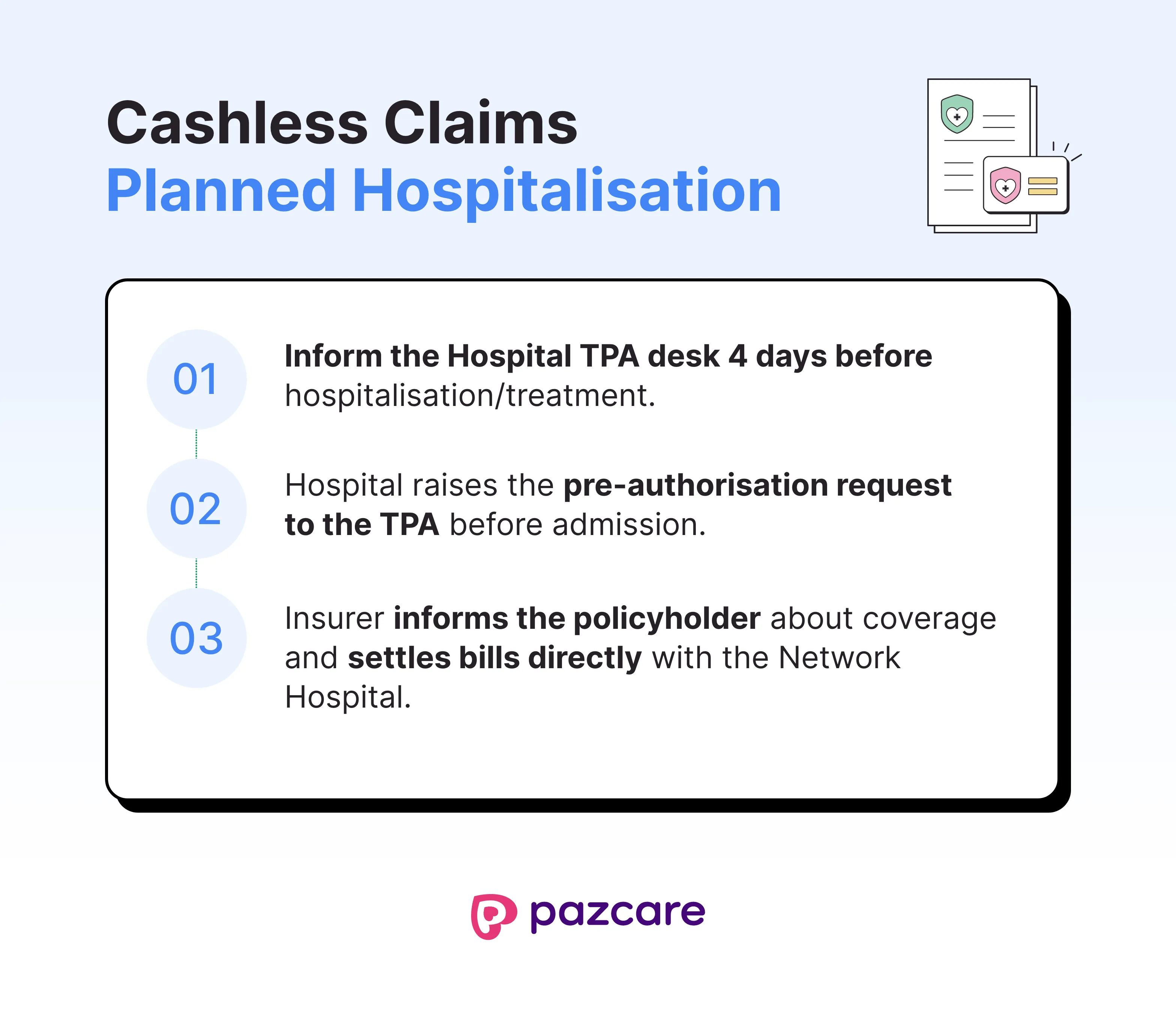

Cashless claim process for planned hospitalization

Inform the insurer at least 4 days before the treatment/hospitalization date. You can contact the toll-free number of the insurance provider.

After the admission to the hospital, the hospital will fill the pre-authorization form and fax or email it to the insurer after the policyholder submits the valid proof.

Once the process is complete, the insurance company will inform about the coverage provided to the policyholder and the network hospital.

After all of this, the insurance company will settle the bills to the network hospital.

Reimbursement claim procedure

The reimbursement claims can be initiated in a hospital of your choice. The general procedure includes

The insured or the policyholder has to pay all the medical bills and other costs involved in the hospitalization. Make sure you keep all the bills safely for the claim.

Submit the original bills to the insurer along with a duly filled claim form. The claim forms are mostly available on the website of the insurer or their offices.

After this, the claim request is verified and processed according to the terms and conditions of the policy.

Once the claim is verified and the bills are credible the insurer settles the payment to the account of the policyholder.

Documents required for health insurance claim

Duly filled claim form. Available on the website or the offices of the insurer.

A health insurance ID card provided by the insurer.

A valid unique identity card like Aadhar, Voter Id, etc.

All the original medical bills and pharmacy bills.

Doctor consultation and prescription papers.

Investigation report

Discharge summary from the hospital.

A medical certificate signed by the doctor in charge.

For accidents, FIR or MLC (Medico Legal Certificate) copy

Other relevant documents.

Claim authorization in health insurance

Immediately after the policyholder or the attendant of the insured intimates the claim to the insurance provider, the insurer verifies the policy and the coverage of that policy.

After the verification process by a field doctor, the pre-authorization form is submitted and the cashless claims are approved.

This authorization process can even get canceled if the details mentioned are incorrect.

The claims must be filed within 30 days of discharge from the hospital and intimated at least 4 days before the planned hospitalization.

The insured will have to pay for all other expenses which are not covered under their health insurance policy.

Mostly Third Party Administrators or TPA in health insurance verify the documents and claims. Any claims that are invalid or the details provided are incorrect are rejected.

Health insurance claim rejection common reasons and how to avoid them

One of the most frustrating experiences for any policyholder is getting a health insurance claim rejected especially during a medical emergency. Understanding the common reasons behind claim rejections can help you avoid unnecessary delays or financial stress.

Here are the most frequent causes of claim rejection in health insurance:

Incomplete or incorrect details in the claim form Even small errors such as mismatched names, wrong policy numbers, or missing details can lead to rejection. Always double-check your claim form before submission.

Unclear or fake medical bills Insurers verify every bill and report submitted. Handwritten, illegible, or fabricated bills raise red flags and can result in claim denial.

Policy exclusions Claims made for conditions or treatments that fall under policy exclusions (like pre-existing diseases not yet covered, cosmetic surgery, or dental care) are often rejected.

Late intimation to the insurer Every insurer has a specific time limit for informing them about hospitalization usually within 24 hours for emergencies or 3–4 days for planned admissions. Missing this window can lead to claim rejection.

Non-network hospital admission (for cashless claims) Cashless facilities are available only at network hospitals that have tie-ups with the insurer. If you’re admitted to a non-network hospital, your cashless claim may be denied though you can still apply for reimbursement later.

Pro Tip: Before getting admitted, always verify if the hospital is part of your insurer’s network list and ensure your treatment is covered under the policy. This simple step can prevent unnecessary claim rejections.

What are the 2 types of health insurance claims available?

The two types of health insurance claims are cashless claims and reimbursement claims. A cashless claim is where the insurer settles the claim amount directly to the network hospital. In a reimbursement claim, the policyholder settles the claim amount out of his/her pockets and later the insurer settles the bill to their bank account.

How is claim settlement done in health insurance?

The process for settling health insurance claims is as follows:

The policyholder initiates a health insurance claim. If admitted to a network hospital, a cashless claim can be initiated; otherwise, a reimbursement claim is initiated.

For cashless claims, the insurer settles the claim directly with the network hospital.

For reimbursement claims, the policyholder submits necessary documents like claim forms and discharge summaries to the in-house claims team or Third-Party Administrator (TPA) for verification. Once approved, the claim amount is directly settled into the insured's bank account.

Claims must be filed within 30 days of hospital discharge and must be intimated at least 4 days before planned hospitalization.

The insured is responsible for all expenses not covered under their health insurance policy.

What is a claim in insurance?

A claim is a request made to an insurance company to cover the cost or expense incurred during the treatment of a medical condition that is covered by them the insurance policy.

When should I apply for reimbursement claims?

After discharge from the hospital, the claims form must be submitted within 15 days (or as mentioned in terms and conditions) to the insurer.

What are the documents required to claim reimbursement?

You need to show valid ID proof, a health ID card, and all original medical bills from the hospital to apply for a reimbursement claim.

What are the documents required for making a cashless claim?

In the case of a cashless claim, the insured shows the health insurance card and a valid identity proof to the network hospital. After that the hospital submits a pre-authorization form to the insurer to initiate the cashless claim.

.webp)

.svg)

.svg)