Why is your group health insurance claim not fully settled?

Learn why your group health insurance claim is not fully settled. Explore common reasons, deductions, and tips to avoid partial claim payouts.

Team Pazcare

This is some text inside of a div block.

Updated on:

March 24, 2026

Share

Table of Contents

Key Takeaways

Explore the common reasons why your group health insurance claims are not fully settled, such as non-medical expenses, policy changes, and various caps.

This article emphasizes the need for regular policy reviews to prevent unexpected financial burdens and offers practical insights for better insurance understanding.

Explore the common reasons why your group health insurance claims are not fully settled, such as non-medical expenses, policy changes, and various caps.

This article emphasizes the need for regular policy reviews to prevent unexpected financial burdens and offers practical insights for better insurance understanding.

Many people submit claims without realising that their group health insurance policy might not cover everything. As a result, some parts of the claims get resolved, while others do not. This often leads to situations where claims are only partially settled. This piece will explore the typical reasons behind partial claim settlements in group health insurance, along with examples.

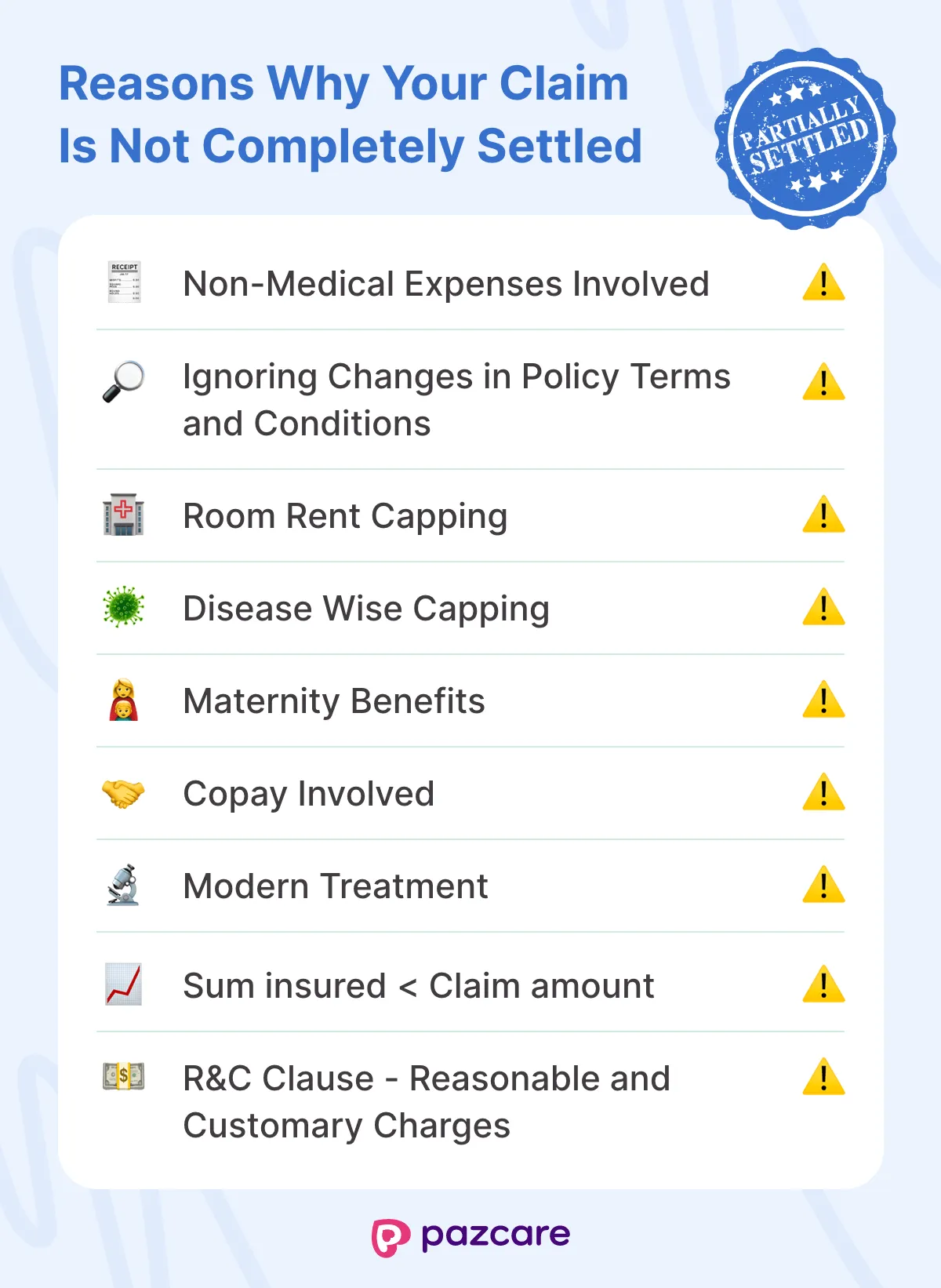

9 Reasons Why Your Claim Is Not Completely Settled

Non-Medical Expenses Involved

Tarun underwent medical treatment and submitted a cashless claim. However, the insurer covered only 95% of the medical bill. The remaining 5%, which included non-medical expenses like gloves, cotton, admin fees, registration fees, etc., was not covered under the Group Health Insurance Policy. Consequently, Tarun had to personally cover these non-medical expenses.

During the claim settlement process, numerous insurers may have exclusions in group health insurance, they are non-medical expenses such as tissues, gowns, gloves, handwash, or cotton used during a patient's hospital admission. Patients are typically expected to cover these expenses themselves.

Ignoring Changes in Policy Terms and Conditions

Saanvi had a Group health insurance policy with a 'No Copay' feature last year. However, when she filed a surgery claim this year, she was unexpectedly required to pay a 10% copay. Saanvi was unaware that her organisation had changed the policy terms during renewal. This experience made her realise the importance of regularly checking policy terms to prevent future surprises.

Room Rent Capping

Consider Aman, with a group health insurance coverage of 5 lakhs and a daily room rent allowance of 1% for normal rooms and 2% for ICU. This implies that his room rent is limited to 5,000 per day for a normal hospital room and 10,000 per day for an ICU. Once during hospitalisation, he opted for a normal room priced at 8,000 per day. When he filed a claim for the total amount, the claim was partially approved. Exceeding the room rent limit by 3,000 resulted in an out-of-pocket expense for him, with a proportionate deduction.

Therefore, it is important to check your group insurance policy's room rent capping and adhere to it to prevent partial claim settlements.

Disease Wise Capping

Swathi has a group health insurance coverage of 3 lakh, but she is unaware of the disease-specific limits outlined in the policy. She underwent cataract surgery for one eye which cost her 30,000. When she filed a claim with the insurer, the insurer notified her that certain diseases have predetermined maximum payouts. In her case, the cataract maximum payout is 20,000 and hence, only 20,000 of her claim will be approved.

Learn from Swathi. Always review your group health insurance policy, including disease-specific limits and maximum payouts for each ailment to avoid such situations.

Maternity Benefits

Ria underwent a C-section labour which cost her 75,000. However, her group health insurance had a maternity benefit limit of 50,000. Hence, the insurer covered only 50,000, and she had to bear the remaining cost.

Many insurers cap maternity-related expenses at 50,000, with a few extending it to 1,00,000. It's crucial to know your insurance company's limits for such expenses.

Copay Involved

Ravi holds a group health insurance policy of 3 lakh coverage with a 20% copay. He underwent a treatment costing 10,000, resulting in a copay of 2,000 (20% copay) from his pocket, while the insurance company covered the remaining 8,000.

A copay represents a percentage or fixed amount that you must pay against the medical expenses while the insurance company settles the remaining amount. However, some policies have a 'No Copay' option too. It's essential to review the policy terms and conditions provided by the insurance company to determine if a copay is applicable.

Modern Treatment

Jayanth needed cardiac surgery, and the doctors advised him to a robotic surgery. Since IRDAI has mandated all health insurance to cover modern treatments in their policy, he assumed that this would be completely covered under his group health insurance policy. However, he later discovered that his policy only covered 50% of the sum insured for such treatments. Consequently, he had to cover the remaining amount for the surgery.

Sum insured < Claim amount

Akash utilized 3 lakhs from his 4 lakh company-provided sum insured for himself and his family in a single year. His recent hospital stay cost him 1,50,000. He filed a claim for the entire amount without realizing he had reached the limit. As a result, he received only the remaining sum insured, and he had to cover the remaining expenses.

This teaches us to always monitor our sum insured during multiple hospitalizations or if our claim exceeds the sum insured to avoid unexpected financial burdens.

R&C Clause - Reasonable and Customary Charges

Rahul, aged 55 years old, undergoes a heart surgery. His hospital bills him 6 lakhs. He files a claim with his group health insurance company. But when the insurer checks the bills, they discover that the hospital has overcharged, and the reasonable and acceptable cost for the surgery in that locality is only 4 lakhs. Consequently, the insurer covers only 4 lakh, leaving Rahul responsible for the remaining amount.

Insurance companies have a 'Reasonable and Customary Clause' in their policies to protect themselves from having to pay unreasonable and excessive hospital bills. It's the amount of money your health insurance company thinks is fair for a specific medical service or procedure.

Where in the claim journey do deductions happen in a group health insurance policy?

Understanding when deductions happen in a group health insurance can help employees avoid surprises and better utilize their group insurance for employees.

In a group health insurance plan, the claim journey often begins with pre-authorization, especially for cashless treatment at a network hospital. Here, the insurer or TPA approves a certain amount based on your group health insurance cover.

This approved amount may not reflect the final bill. Factors like policy limits, sub-limits, and exclusions under your group health insurance policy can already start impacting the claim.

Tip: Always check the initial approval amount and understand what is included to avoid surprises later.

2. During hospitalization (Non-Payables Added)

During treatment, hospitals add various consumables and administrative charges that may not be covered under your group health insurance cover.

Even the best group health insurance policy in India may exclude such non-medical expenses unless additional coverage is provided.

Tip: Ask for interim bills to track non-payable items in real time.

3. Final settlement stage

At the final stage, insurers assess the claim based on:

Here’s how Pazcare helps employees and HR teams get the most out of their group health insurance cover:

Policy dashboard

Clear visibility into what your group health insurance policy covers, including limits, exclusions, and benefits.

Real-time sum insured tracking

Employees can track their available coverage, reducing the risk of exceeding limits under their group insurance for employees.

Claim assistance

Dedicated support to help employees navigate claims, resolve issues, and minimise deductions.

Employee education

Regular guidance and resources to help teams understand their group health insurance plan better and avoid common mistakes.

Wrapping Up

As a policyholder, you expect financial security as you constantly pay your group health insurance premiums. However, certain aspects of claims may occasionally not be covered for various reasons outlined above. It's vital to keep these considerations in mind to avoid unforeseen financial strains and ensure you receive the coverage you're entitled to.

Key takeaways

Blog sources

About the Author

Follow on:

Thanks for subscribing! If it’s your first time, check your inbox. Otherwise, you’re already on our list

Oops! Something went wrong while submitting the form.

Ready to give yourself and your team the best employee benefit experience?

The claim amount is sent to the verified nominee’s bank account.

What is a good claim settlement ratio?

A good claim settlement ratio is usually above 90%. Insurers with ratios above 95% are generally considered very reliable in settling claims.

How does claim data affect renewal pricing?

Insurers assess your claim ratio, high-cost treatments, and recurring claims before revising premiums. Analyzing this data in advance allows HR teams to restructure the group health insurance cover, introduce cost controls, and negotiate from a stronger position.

Does cashless claim mean no sub limit?

No. Cashless hospitalization does not remove sub limits. The same caps apply during cashless claims.

Can HR simplify the claims experience?

Yes. HR plays a crucial role in providing clarity, tools, and guidance to help employees through it.

.svg)

.svg)